12 |

Oilfield Technology

September 2016

At a national level, NOCs are establishing dedicated oil and gas R&D

facilities. For instance, the AbuDhabi National Oil Company (ADNOC) is in

the final stages of inaugurating its Petroleum Institute research centre in

AbuDhabi. They are also playing amore significant role in the integration

of the oil and gas innovation ecosystem into that of their home economies.

Indeed, NOCs are creating effective linkages between their own in-house

R&D centres and other research and academic institutions, service

companies, and external universities. These linkagesmake the innovation

ecosystemwork, thereby promoting theNOCs’ innovation agenda and

meeting their business needs. Moreover, NOCs are taking on amore

active role in establishing technology parks to create forums that bring

partners and academic institutions closer to theNOCs’ operation sites.

Saudi Aramco for example is actively shaping the vision of the Dhahran

Techno-Valley to attractmajor oil and gas players.

At an international level, NOCs are also expanding their investments

in physical oil and gas R&D facilities. Saudi Aramco recently opened a

research centre inDetroit, its eighth satellite research facility and its third in

theUS. Additionally, NOCs are strengthening their portfolio of relationships

by establishing large-scale strategic collaboration agreementswith

external parties. By doing so, they are delivering specific R&Dprojects,

advancing their own capability development and increasingly

participating in shaping the global discussion on oil and gas R&D and

innovation. Notable examples areQatar Petroleum’s collaborationwith

Imperial College London in theQatar Carbonate and Carbon Storage

Research Centre and Saudi Aramco’s Aramco Fuel Research Center created

in collaborationwith France’s IFP Energies Nouvelles (IFPEN).

Risingtothechallenge

AlthoughNOCs have laid the foundations, building innovation capabilities

requires addressing several region-specific challenges. These include the

limited nature of local innovation ecosystems in the oil and gas sector,

insufficient governmental support for R&D, the scarcity of research

talent, weak links between academia and industry, and the predominant

workplace culture of sourcing technologies fromexternal suppliers rather

than developing in-house solutions. Middle East NOCs can overcome these

problems by using a framework that proceeds fromdefining a strategy to

establishing the appropriate innovation culture (Figure 3). Along theway,

it is crucial for themto understand that building R&D capabilities is not

about creating another cost centre. Rather, R&D capabilities

offermany opportunities to generate returns in the long term

and, very often, in the short term.

DefineaclearR&Dstrategy

NOCsmust start by defining a clear R&D strategy that is

tailored to their business needs. The strategywill therefore

depend on eachNOC’s upstreamand downstream

specificities and aspirations. For instance, upstream

R&D tends to focus on country-specific challengeswhile

downstreamR&Doften tackles challenges common to

several NOCs and international oil companies. Bearing

those specificities inmind, NOCswill require clarity on their

R&Dmandate, their R&D focus, and their ambitions for R&D

capabilities. NOCs need to agree onwhether the company’s

mandate is to promote R&D efforts at a company level or

at a broader country level. Once this has been decided, it is

essential to identify and prioritise areas that are critical for the

success of long-termbusiness strategies andNOCs’ agreed

national mandates. After that, NOCs should clearly outline

their capability ambitions. Thismeans specifying inwhich

areas theywill simply adopt the best available technologies

fromexternal suppliers and inwhich areas theywill develop

in-house capabilities and solutions. The R&D strategy then

needs to be stress-tested to ensure that it can survivemarket

volatility and uncertainties. Furthermore, and as part of

their strategy definition efforts, NOCs need a set of portfolio

management tools, systems, and processes that will lead

to transparency in the R&Dportfolio and propermonitoring

of R&D activities. R&Dportfoliosmust address current and

future business and technology requirements. In addition,

R&Dportfolios should possess an optimal risk profilewith a

mix of lower risk, often short-term, projects and higher-risk,

often longer-term, projects.

Buildafit-for-purposeoperatingmodel

NOCsmust define the right organisational model, governance

framework, processes and decision rights if they are to build

a fit-for-purpose R&Doperatingmodel. To achieve this, the

R&D functionmust be positioned so that it fosters strong

linkages between the development and deployment of new

technologies, enhances cross-disciplinary collaboration, and

ensures seniormanagement ownership of the R&D agenda.

Figure 2.

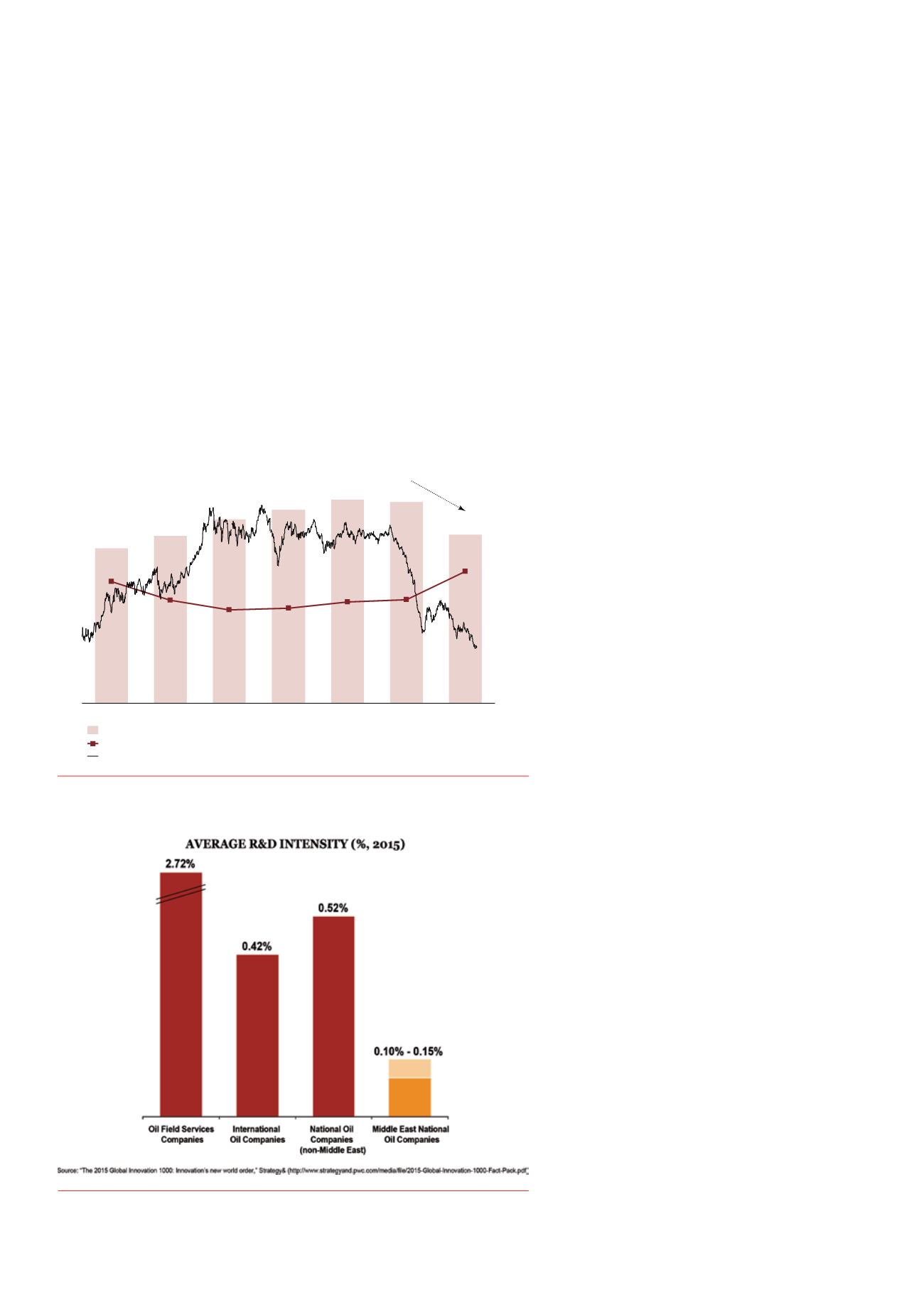

Middle East NOCs lagbehind the rest of the industry in research intensity.

Figure 1.

Oil andgas R&D intensity is rising, despite broader falls inR&D spending.

11.4

13.6

13.7

13.0

12.4

11.3

10.4

1.0

0.9

0.8

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0.0

2015

0.55%

2014

0.44%

2013

0.43%

2012

-16%

0.40%

2011

0.39%

2010

0.43%

2009

0.51%

Overall R&D Intensity (%)

Overall R&D spending (US$ billion)

Brent Oil Price (US$)

0

10

20

30

40

50

60

70

80

90

100

110

120

130

US$/barrel

R&D

intensity (%)

Exhibit 1

Oil and gas R&D intensity is rising, despite broader falls in R&D spending

Note: R&D intensity is the ratio of R&D spending to revenues

Source: “The 2015 Global Innovation 1000: Innovation's new world order,” Strategy&

(

, Strategy& analysis